by Dwaipayan Bose

Small and midcap funds have attracted a huge amount of retail investor interest over the last 3 years. Over this period small and midcap funds have outperformed large cap and flexi cap (diversified) funds across different market conditions. While there are some concerns regarding midcap valuations, historical data shows that, midcap funds usually give higher returns than large cap funds over a long investment horizon. As such, in our view, small and midcap funds should form a part of the long term equity portfolios, especially for young investors.

I have seen that, many investors and financial advisors select mutual fund schemes based on recent performance; at any point of time, there are 5 or 6 funds, which are high on the shopping list of investors. However, you should know that, recent performance is not a good indicator of future performance. Over the last 15 years I have seen many erstwhile top performing mutual funds languishing in lower performance quartiles for long periods of time. In the case of midcap funds there is usually a big gap in performance between the best performers and the poor performers. Therefore, you must select midcap funds wisely. In this post, we will discuss how to select the best midcap funds.

Recent outperformance can be misleading

Let us first discuss why you should not select small / midcap funds just based on recent performance. Large cap stocks usually have higher correlation with major indices, e.g. Nifty, Sensex, BSE 100, Nifty 100 etc, but some midcap stocks may show a wide divergence from the performance of major indices. Midcap stocks giving more than 100% returns in a year are not unheard of. If a mutual fund scheme’s portfolio is concentrated in a few of such multi-bagger stocks, then it can give outstanding returns during a particular period.

You should, however, understand that, such extraordinary returns cannot be sustained because after a spectacular rally such stocks can become overvalued and investors are likely to lose interest in the stock. If a midcap fund’s performance is largely attributed to the rally of a few multi-bagger stocks, then its performance is likely to be average or below average once such stocks cool off after the big rally. Therefore, recent strong performance of a small / midcap fund can be misleading.

Qualities of the fund manager is the most important parameter

The performance of a mutual fund scheme can be attributed to three factors, (a) the overall market performance, (b) the risk taken by the fund manager and (c) the value-added by the fund manager (also known as alpha). Over a sufficiently long investment horizon, the last factor is the most important one. It is especially important in the case of small / midcap funds because, unlike large cap stocks, midcap and small cap stocks are under-researched in the public domain. Therefore, fund managers, who have deep knowledge of the business through experience of investing in similar companies, factory / site visits, and discussions with management etc., backed up by strong research capabilities of the Asset Management Company have an edge in delivering higher alphas.

Some of our readers may ask that, how will an average retail investor know if a fund manager has these outstanding qualities which enable him or her to deliver superior returns to investors compared to others? It is a fair question. Fund managers often give interviews in electronic (TV) and digital media. We, in Advisorkhoj, follow these interviews and also interview fund managers on our own website from time to time. We urge to readers to go through the interviews of Fund Managers / Chief Investment Officers on our website. However, we recognize that, investors may not have the time or sufficient information (fund managers are often constrained in terms of what they can or cannot speak to the media). So in interest of our readers, we have developed some analytical tools on our website that, will give investors a sense of how well the fund manager of a scheme has performed relative to others. Investors can use these tools in their fund selection.

Consistent Performance

Consistency in performance is the hallmark of a good fund manager and it should be one of the most important, if not the most important, fund selection criteria. Consistency in performance shows that, the scheme performed well in different market conditions over a period of time. Returns over the last 1 year or 3 years (trailing returns), often masks poor performance in an interim or different period, if the recent market conditions are highly favourable to the investment strategy of the fund manager.

In advisorkhoj.com we have built an analytical tool, Top Consistent Mutual Fund Performers, using which you can identify schemes which have performed most consistently in the last 5 years. Our internal research has shown that, 5 years is the best period for measuring performance consistency because a 5 year period usually has periods of rising market and falling market; therefore it covers different market conditions.

In the tool, Top Consistent Mutual Fund Performers, we look at a scheme’s performance in each year over the past 5 years. We then rank the scheme’s annual performance in performance quartile, Top Quartile has the best performers, Upper Middle Quartile has the next best above average performers, Lower Middle Quartile has the below average performers and Bottom Quartile has the poorest performers in any year. Using our proprietary ranking methodology, we then rank mutual fund schemes in different categories in terms of performance consistency. We urge our readers to use this tool, to identify the most consistent mutual fund performers.

Rolling Returns

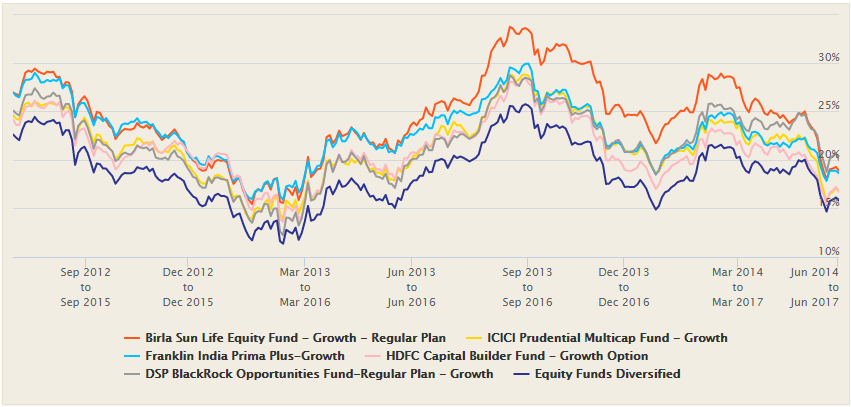

In our tool, Top Consistent Mutual Fund Performers, we identified most consistently performing top funds using annual relative performance across different market conditions. Regular readers of our blog will be aware that, rolling returns is the best analytical measure of a fund’s performance consistency. In rolling returns, we look at the annualized returns of a fund for specific investment tenures, on every day over a specified period. Usually, the results are shown in a graphical (chart format). In Advisorkhoj, we also show summary of important rolling return analytics in a tabular format.

You can see the rolling return performance of an individual scheme versus the category (Equity Funds Small and Midcap for the purpose of this post), using our tool, Rolling Return vs Category. You can also compare rolling returns performance of multiple schemes by clicking on the link Add another fund; you can compare up to four funds. In the table below the chart, you can see the important Rolling Return analytics like Average Rolling Returns, Median, Rolling Returns, Maximum Rolling Returns and Minimum Rolling Returns. We also show Return Consistency in the table; i.e. how much percentage of times in the chosen period the rolling returns of the fund were in the specific rolling return ranges.

When using this tool for equity funds, especially small and midcap funds, we recommend that, investors choose a rolling return of at least 3 years, because in our view, investors should have at least 3 year investment tenure for equity funds, especially small / midcap funds. If you want, you can choose longer investment tenures; however, very long investment tenures like 10 years may not be relevant for scheme selection because many things may change in 10 years, like fund manager of the scheme, market place dynamics in an evolving market like India, AMC merger and acquisitions etc. We also recommend that, you select a start date that is at least 5 years from the date when you are using the tool because, as discussed earlier, 5 years is the best period for measuring performance consistency; you can choose an older start date if you want.

How to use this tool for fund selection?

You need to shortlist 4 or 5 funds using our Top Consistent Mutual Fund Performers or funds recommended by your financial advisor or any other method. Compare the rolling returns of the funds either graphically or by comparing different performance parameters in the table below. Then you can downsize your shortlist to 1 or 2 funds (or more, as per your needs) based on average, median, minimum or percentage of occurrence in return range that you prefer.

Market Capture Ratio

Market Capture Ratio is, in our view, one of the most important performance metrics of a mutual fund scheme. This metric tells us how a fund performed in up market and down market. This metric provides very useful insights on the risk taken by a fund manager (very important for midcap funds because they are more risky than large cap funds) and also how the stock selection of the fund manager performs in both up market and down market (again very important for midcap funds because these funds usually show divergence from market index performance). You can see market capture ratio of any scheme by using our tool, Market Capture Ratio.

There are two important parameters in Market Capture Ratio - Up Market Capture Ratio and Down Market Capture Ratio. Up Market Capture Ratio measures the percentage of market gains captured by a fund manager when markets are up. If Up Market Capture Ratio is more than 100%, it means the fund manager was able to beat the market benchmark in upturns. I fit is less than 100%, it means that the fund manager was not able to beat the market benchmark in upturns. Down Market Capture Ratio measures the percentage of market losses suffered by your scheme when markets were down. If Down Market Capture Ratio of a scheme is less than 100%, it means that the fund fell less than the market benchmark in downturns.

Down Market Capture Ratio can sometimes be negative. Do not worry if it is negative because negative Down Market Capture Ratio implies that, the fund NAV went up when the market fell. Negative “Down Market Capture Ratio” shows great bottom up stock picking skills of the fund manager. Investors should look at both the Up Market Capture Ratio and Down Market Capture Ratio for true evaluation of fund performance. You should select schemes which have high Up Market Capture Ratio (more than 100%) and low (even negative) Down Market Capture Ratio.

How to use this tool for your fund selection?

Usually the funds selected using our tools Top Consistent Mutual Fund Performers and Rolling Return vs Category should have excellent Up Market and Down Market Capture Ratio. Nevertheless, you can use this tool to verify, if the funds selected by you performed well in both up markets and down markets; fine tune your selection, based on the results of Market Capture Ratio analysis of your selected schemes.

Conclusion

In this post, we discussed several analytical tools for selecting best small / midcap mutual fund schemes for long term investment. We urge our readers to use and play around with these Research tools on our website. We have tried to make these tools as user friendly as possible and we hope that, you will be able to learn to use these tools in a very short time. If you have a good understanding of these tools, you will realize that, in all these tools we are trying to evaluate the fund manager’s performance in different market conditions. In addition to these tools, you can also use star ratings issued by different mutual fund research firms; when using star ratings, you should try to understand how the ratings work. While we want to empower our readers with knowledge of mutual funds, in case you have any doubt, you should consult with your financial advisor before investing. (Courtecy: Advisors Khoj)

Mutual Fund Investments are subject to market risk, read all scheme related documents carefully.

Small and midcap funds have attracted a huge amount of retail investor interest over the last 3 years. Over this period small and midcap funds have outperformed large cap and flexi cap (diversified) funds across different market conditions. While there are some concerns regarding midcap valuations, historical data shows that, midcap funds usually give higher returns than large cap funds over a long investment horizon. As such, in our view, small and midcap funds should form a part of the long term equity portfolios, especially for young investors.

I have seen that, many investors and financial advisors select mutual fund schemes based on recent performance; at any point of time, there are 5 or 6 funds, which are high on the shopping list of investors. However, you should know that, recent performance is not a good indicator of future performance. Over the last 15 years I have seen many erstwhile top performing mutual funds languishing in lower performance quartiles for long periods of time. In the case of midcap funds there is usually a big gap in performance between the best performers and the poor performers. Therefore, you must select midcap funds wisely. In this post, we will discuss how to select the best midcap funds.

Recent outperformance can be misleading

Let us first discuss why you should not select small / midcap funds just based on recent performance. Large cap stocks usually have higher correlation with major indices, e.g. Nifty, Sensex, BSE 100, Nifty 100 etc, but some midcap stocks may show a wide divergence from the performance of major indices. Midcap stocks giving more than 100% returns in a year are not unheard of. If a mutual fund scheme’s portfolio is concentrated in a few of such multi-bagger stocks, then it can give outstanding returns during a particular period.

You should, however, understand that, such extraordinary returns cannot be sustained because after a spectacular rally such stocks can become overvalued and investors are likely to lose interest in the stock. If a midcap fund’s performance is largely attributed to the rally of a few multi-bagger stocks, then its performance is likely to be average or below average once such stocks cool off after the big rally. Therefore, recent strong performance of a small / midcap fund can be misleading.

Qualities of the fund manager is the most important parameter

The performance of a mutual fund scheme can be attributed to three factors, (a) the overall market performance, (b) the risk taken by the fund manager and (c) the value-added by the fund manager (also known as alpha). Over a sufficiently long investment horizon, the last factor is the most important one. It is especially important in the case of small / midcap funds because, unlike large cap stocks, midcap and small cap stocks are under-researched in the public domain. Therefore, fund managers, who have deep knowledge of the business through experience of investing in similar companies, factory / site visits, and discussions with management etc., backed up by strong research capabilities of the Asset Management Company have an edge in delivering higher alphas.

Some of our readers may ask that, how will an average retail investor know if a fund manager has these outstanding qualities which enable him or her to deliver superior returns to investors compared to others? It is a fair question. Fund managers often give interviews in electronic (TV) and digital media. We, in Advisorkhoj, follow these interviews and also interview fund managers on our own website from time to time. We urge to readers to go through the interviews of Fund Managers / Chief Investment Officers on our website. However, we recognize that, investors may not have the time or sufficient information (fund managers are often constrained in terms of what they can or cannot speak to the media). So in interest of our readers, we have developed some analytical tools on our website that, will give investors a sense of how well the fund manager of a scheme has performed relative to others. Investors can use these tools in their fund selection.

Consistent Performance

Consistency in performance is the hallmark of a good fund manager and it should be one of the most important, if not the most important, fund selection criteria. Consistency in performance shows that, the scheme performed well in different market conditions over a period of time. Returns over the last 1 year or 3 years (trailing returns), often masks poor performance in an interim or different period, if the recent market conditions are highly favourable to the investment strategy of the fund manager.

In advisorkhoj.com we have built an analytical tool, Top Consistent Mutual Fund Performers, using which you can identify schemes which have performed most consistently in the last 5 years. Our internal research has shown that, 5 years is the best period for measuring performance consistency because a 5 year period usually has periods of rising market and falling market; therefore it covers different market conditions.

In the tool, Top Consistent Mutual Fund Performers, we look at a scheme’s performance in each year over the past 5 years. We then rank the scheme’s annual performance in performance quartile, Top Quartile has the best performers, Upper Middle Quartile has the next best above average performers, Lower Middle Quartile has the below average performers and Bottom Quartile has the poorest performers in any year. Using our proprietary ranking methodology, we then rank mutual fund schemes in different categories in terms of performance consistency. We urge our readers to use this tool, to identify the most consistent mutual fund performers.

Rolling Returns

In our tool, Top Consistent Mutual Fund Performers, we identified most consistently performing top funds using annual relative performance across different market conditions. Regular readers of our blog will be aware that, rolling returns is the best analytical measure of a fund’s performance consistency. In rolling returns, we look at the annualized returns of a fund for specific investment tenures, on every day over a specified period. Usually, the results are shown in a graphical (chart format). In Advisorkhoj, we also show summary of important rolling return analytics in a tabular format.

You can see the rolling return performance of an individual scheme versus the category (Equity Funds Small and Midcap for the purpose of this post), using our tool, Rolling Return vs Category. You can also compare rolling returns performance of multiple schemes by clicking on the link Add another fund; you can compare up to four funds. In the table below the chart, you can see the important Rolling Return analytics like Average Rolling Returns, Median, Rolling Returns, Maximum Rolling Returns and Minimum Rolling Returns. We also show Return Consistency in the table; i.e. how much percentage of times in the chosen period the rolling returns of the fund were in the specific rolling return ranges.

When using this tool for equity funds, especially small and midcap funds, we recommend that, investors choose a rolling return of at least 3 years, because in our view, investors should have at least 3 year investment tenure for equity funds, especially small / midcap funds. If you want, you can choose longer investment tenures; however, very long investment tenures like 10 years may not be relevant for scheme selection because many things may change in 10 years, like fund manager of the scheme, market place dynamics in an evolving market like India, AMC merger and acquisitions etc. We also recommend that, you select a start date that is at least 5 years from the date when you are using the tool because, as discussed earlier, 5 years is the best period for measuring performance consistency; you can choose an older start date if you want.

How to use this tool for fund selection?

You need to shortlist 4 or 5 funds using our Top Consistent Mutual Fund Performers or funds recommended by your financial advisor or any other method. Compare the rolling returns of the funds either graphically or by comparing different performance parameters in the table below. Then you can downsize your shortlist to 1 or 2 funds (or more, as per your needs) based on average, median, minimum or percentage of occurrence in return range that you prefer.

Market Capture Ratio

Market Capture Ratio is, in our view, one of the most important performance metrics of a mutual fund scheme. This metric tells us how a fund performed in up market and down market. This metric provides very useful insights on the risk taken by a fund manager (very important for midcap funds because they are more risky than large cap funds) and also how the stock selection of the fund manager performs in both up market and down market (again very important for midcap funds because these funds usually show divergence from market index performance). You can see market capture ratio of any scheme by using our tool, Market Capture Ratio.

There are two important parameters in Market Capture Ratio - Up Market Capture Ratio and Down Market Capture Ratio. Up Market Capture Ratio measures the percentage of market gains captured by a fund manager when markets are up. If Up Market Capture Ratio is more than 100%, it means the fund manager was able to beat the market benchmark in upturns. I fit is less than 100%, it means that the fund manager was not able to beat the market benchmark in upturns. Down Market Capture Ratio measures the percentage of market losses suffered by your scheme when markets were down. If Down Market Capture Ratio of a scheme is less than 100%, it means that the fund fell less than the market benchmark in downturns.

Down Market Capture Ratio can sometimes be negative. Do not worry if it is negative because negative Down Market Capture Ratio implies that, the fund NAV went up when the market fell. Negative “Down Market Capture Ratio” shows great bottom up stock picking skills of the fund manager. Investors should look at both the Up Market Capture Ratio and Down Market Capture Ratio for true evaluation of fund performance. You should select schemes which have high Up Market Capture Ratio (more than 100%) and low (even negative) Down Market Capture Ratio.

How to use this tool for your fund selection?

Usually the funds selected using our tools Top Consistent Mutual Fund Performers and Rolling Return vs Category should have excellent Up Market and Down Market Capture Ratio. Nevertheless, you can use this tool to verify, if the funds selected by you performed well in both up markets and down markets; fine tune your selection, based on the results of Market Capture Ratio analysis of your selected schemes.

Conclusion

In this post, we discussed several analytical tools for selecting best small / midcap mutual fund schemes for long term investment. We urge our readers to use and play around with these Research tools on our website. We have tried to make these tools as user friendly as possible and we hope that, you will be able to learn to use these tools in a very short time. If you have a good understanding of these tools, you will realize that, in all these tools we are trying to evaluate the fund manager’s performance in different market conditions. In addition to these tools, you can also use star ratings issued by different mutual fund research firms; when using star ratings, you should try to understand how the ratings work. While we want to empower our readers with knowledge of mutual funds, in case you have any doubt, you should consult with your financial advisor before investing. (Courtecy: Advisors Khoj)

Mutual Fund Investments are subject to market risk, read all scheme related documents carefully.